Background

The U.S. Postal Service is an independent establishment of the executive branch. It generates its cash almost entirely by selling postal products and services. The Postal Service has reached its statutory borrowing limit of $15 billion as of September 30, 2012 and cannot borrow additional money to enhance cash flow.

The U.S. Postal Service is an independent establishment of the executive branch. It generates its cash almost entirely by selling postal products and services. The Postal Service has reached its statutory borrowing limit of $15 billion as of September 30, 2012 and cannot borrow additional money to enhance cash flow.

The Postal Service does not have sufficient cash to meet all of its legal obligations, pay down debt, and make critically needed infrastructure investments. Changes to its business model and the laws that govern the Postal Service are needed to reduce financial challenges.

The days of operating cash on hand is a financial ratio that informs an entity and its stakeholders how long the entity can sustain operations if it is unable to generate cash. The calculation divides the total amount of cash on hand, including cash equivalents that can easily be converted to cash, by total daily cash outflow. Daily cash outflow includes daily operating expenses, but not expenses such as depreciation and amortization that do not involve cash.

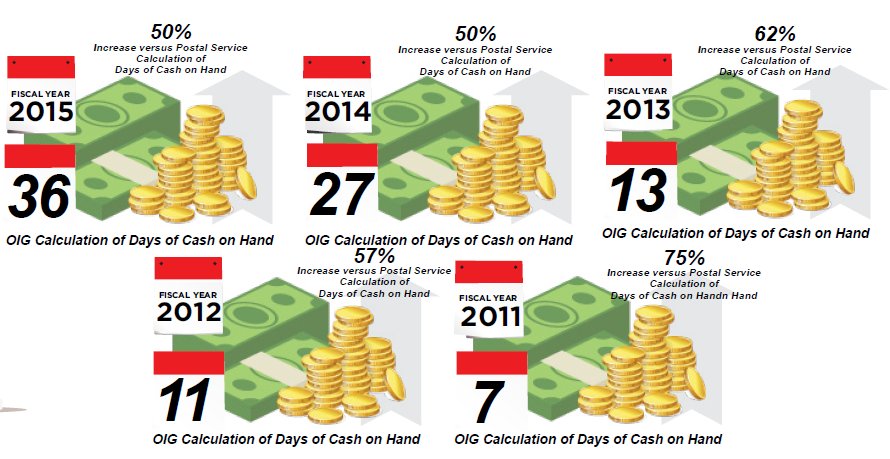

The Postal Service includes days of operating cash on hand in its quarterly and annual financial reports and its integrated financial plans. As of the end of FY 2015, the Postal Service reported 24 days of operating cash on hand.

The objective of this audit was to determine whether the calculation of days of cash on hand was accurate and consistent with other like entities.

What the OIG Found

The Postal Service’s days of cash on hand calculation was not consistent with best practices. If it were done consistently, days of cash on hand would be 36 instead of 24, as reported by the Postal Service. The Postal Service uses banking days of 251 (excludes holidays and weekends) rather than operating days of 365 in its calculation. Additionally, capital outlays are incorrectly included in its calculation, which further dilutes days of cash on hand.

In addition, management, since FY 2013, has not defined the number of days of operating cash on hand needed to sustain operations through a short-term economic downturn. The Postal Service has stated that if it has insufficient cash, it would prioritize paying its employees and suppliers. However, the Postal Service has not defined when these contingency measures should be introduced.

With the inaccurate calculation of days cash on hand and absent a definition when liquidity contingency measures should be initiated, the Postal Service could be increasing its own liquidity risk. Further, the Postal Service could be relying on inaccurate data for critical strategic financial decisions and retaining cash it could otherwise use to improve its financial position. Thus, the Postal Service could use these 12 days (or $1 billion of existing cash) to continue the present approach of saving cash in case of another economic downturn, pay amounts to the Office of Personnel Management for Federal Employee Retirement System or Postal Service Retiree Health Benefits Fund obligations, reduce its debt to the Treasury, or more aggressively fund investments in its infrastructure.

The days of cash on hand method, while standard in the financial analysis community, underestimates the practical level of liquidity the Postal Service has. This standard method assumes identical costs and absolutely no revenue. It can, therefore, be misunderstood by those not familiar with such standard analysis techniques.

What the OIG Recommended

We recommended management calculate and report the number of days of cash on hand using operating days and excluding capital outlays in the calculation. We further recommended management define the number of days of operating cash on hand it should have to sustain operations through a short-term economic downturn.

Read full report

Source: USPS Office of Inspector General