Federal Income Tax Withholding

Effective Pay Period 04-2018, payroll checks will reflect changes in the withholding of federal taxes. All information in this article is based on Internal Revenue Service (IRS) Notice 1036, revised January 2018. The Early Release Copies of the Percentage Method Tables for Income Tax Withholding will appear in IRS Publication 15 (Circular E), Employer’s Tax Guide.

The biweekly personal exemption value for each federal tax allowance changed to $159.60 per allowance. The dollar amounts for the withholding tables and withholding rates (10%, 12%, 22%, 24%, 32%, 35%, and 37%) have also changed (see Federal Income Tax Withholding table).

* Wages are determined after subtracting withholding allowances, CPP, FEDVIP, FEHB, (USPS HB, if pre-tax in place), FSA, HSA, and TSP contributions from your gross earnings.

Employee contributions to the following are treated as pre-tax monies for federal tax computations:

- Commuter Program (CPP) up to the transit and parking pre-tax limits.

- Federal Employees Dental and Vision Insurance Program (FEDVIP).

- Health Benefits (HP):

- Federal Employees Health Benefits (FEHB), unless employee declined the pre-tax benefit.

- USPS Health Benefits (USPS HB), only if employee opted for pre-tax contributions.

- Flexible Spending Accounts (FSA).

- Health Savings Account (HSA).

- Traditional Thrift Savings Plan (TSP).

When calculating your federal taxes, you must subtract the following from your gross earnings to determine your federal taxable wage amount:

- Your withholding allowance amount.

- Your pre-tax contribution amounts.

Upon submission of your federal tax return, review your federal tax withholdings, particularly if you owed a significant amount of money or were due a large refund. If necessary, update your Federal Form W-4 (Employee’s Withholding Allowance Certificate).

To determine the amount of withholding, follow steps 1 through 11:

- Determine the biweekly gross wages from your earnings statement.

- Determine the biweekly Traditional TSP employee contribution from your earnings statement.

- Determine the biweekly FSA contribution from your earnings statement. If applicable, add up the sub-account contributions for the FSA Dependent Child (FSADC) and the FSA Health Care (FSAHC) to determine your total FSA contribution amount.

- Determine the biweekly FEHB pre-tax employee contribution from your earnings statement (abbreviated as HP).

- Determine the biweekly USPS HB pre-tax employee contribution from your earnings statement.

Note: Generally USPS HB contributions are treated as post-tax monies.- Determine the biweekly CPP employee contribution from your earnings statement.

- Determine the biweekly FEDVIP employee contribution from your earnings statement.

- Determine the biweekly HSA contribution from your earnings statement.

- Multiply the number of exemptions claimed by the biweekly exemption value of $159.60 (withholding allowance). The federal tax line on your earnings statement shows the number of exemptions you have claimed (e.g., S1 = single with one exemption, M3 = married with three exemptions).

- Subtract the amounts in step 2 (Traditional TSP), step 3 (FSA), step 4 (FEHB), step 5 (USPS HB, only if pre-tax), step 6 (CPP), step 7 (FEDVIP), step 8 (HSA) and step 9 (exemptions) from step 1 (biweekly gross wages). The balance is the amount subject to withholding.

- Use the Federal Income Tax Withholding table to determine which range your withholding amount falls within; follow the instructions listed in the table.

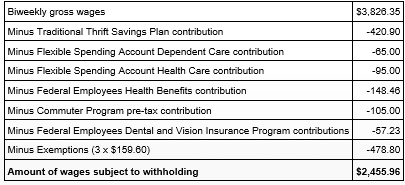

The following is an example of how to compute federal income taxes for a Federal Employee Retirement System (FERS) employee who claims married with three exemptions, and makes pre-tax contributions to the TSP, FSA, FEHB, CPP, and FEDVIP.

A FERS employee receives $3,826.35 as biweekly gross wages. The employee makes the following contributions:

- 11 percent of basic earnings (for this example, all of the gross $ is basic; basic X .11 = $420.90) per pay period (PP) to TSP;

- $65 per PP to FSADC;

- $95 per PP to FSAHC;

- $148.46 per PP to FEHB;

- $105 for this PP to the CPP; and

- $57.23 per PP to a PPO High Option Dental Premium.

The employee claims “married” with three exemptions (M3 on the federal tax line of the earnings statement). Using the information provided in the Federal Income Tax Withholding table in this article, federal taxes are computed as follows:

To complete the computation, refer to the Married segment of the Federal Income Tax Withholding table. The amount of wages subject to withholding ($2,455.96) falls within the “over $1,177 but not over $3,421” range. Using the information provided within that range, the final computation is as follows:

* Rounding may vary this total by a few cents.

— Payroll, Controller, 2-1-18

Source: USPS